How Mythos Mandates Transformation In Financial Crimes Risk Management of European Banking?

Explore how Mythos could change Financial Crimes Risk Management in European banking through faster response cycles.

Financial Crimes Risk Management has traditionally focused on detecting suspicious activity, investigating alerts, and maintaining regulatory compliance through structured operating cycles. The expectation has been that institutions would have enough time to investigate and respond before risk escalated.

Reports surrounding Anthropic’s Mythos model and the European Central Bank’s engagement with all 111 directly supervised euro-zone banks highlighted a new challenge.

The issue now is not just early detection but early response to suspicious activities. Public reporting linked Project Glasswing participants to the discovery of more than 10,000 high and important severity vulnerabilities across widely used software environments.

For European banks, the question that rises now is about operational capacity and resilience when response cycles become shorter than traditional investigation and remediation models.

This article explores what the Mythos usage by money launderers could signal for European banking and why future financial crimes risk management may depend as much on execution and monitoring as on detection.

What Is Mythos and Why Does It Matter for Financial Crimes Risk Management?

Mythos is an advanced cybersecurity AI model developed by Anthropic to identify previously unknown software vulnerabilities and accelerate vulnerability analysis. Through Project Glasswing, Anthropic has made the model available to a limited group of organizations working on defensive cybersecurity, with the goal of strengthening software security before vulnerabilities can be exploited.

The model drew significant attention after reports suggested it could compress vulnerability analysis from weeks to hours. For European banks, the concern was the possibility that threat discovery could begin outpacing the industry's ability to investigate, remediate, and document responses.

This is why Mythos has relevance beyond cybersecurity. Financial Crimes Risk Management relies on timely investigations, evidence collection, decision making, and regulatory reporting. If new threats are identified much faster than institutions can validate exposure and implement controls, operational pressure increases across financial crime, cyber risk, and compliance functions.

The reported discussions involving the European Central Bank and the limited availability of Mythos through Project Glasswing also highlighted another challenge. Banks may be expected to strengthen resilience against threats identified by capabilities they cannot directly access.

Whether Mythos becomes widely available or remains restricted, it signals a broader shift. AI is accelerating how quickly risks can be identified, making operational execution, investigation capacity, and explainable decision making increasingly important components of Financial Crimes Risk Management.

What Does the Mythos Event Reveal About the Future of Financial Crimes Risk Management?

Financial Crimes Risk Management is entering a new operating environment because the speed of risk identification is increasing faster than institutions’ ability to investigate, document, and respond.

Historically, banks improved through stronger detection controls, additional review layers, and larger investigation teams. That model assumed institutions would have enough time to validate findings and maintain governance standards before risks became operationally significant.

Events surrounding Mythos challenge that assumption. Reports linked Anthropic’s restricted Mythos model to large-scale vulnerability discovery and accelerated analysis workflows that compressed activities traditionally measured in weeks into hours or days.

The significance for European banking is not limited to cybersecurity. It introduces a larger question about whether existing operating models can respond at the speed that new risk environments may demand.

Investigation and remediation timelines may compress

Financial Crimes Risk Management depends on time. Alerts need to be reviewed, investigations need evidence and escalations require validation. Decisions must be documented before action is taken.

A vulnerability identified today may require immediate investigation across customers, transaction activity, internal exposure, third parties, and reporting obligations. Teams that previously operated in weekly remediation cycles may find themselves expected to respond within hours. This changes the economics of investigation work as more capacity becomes necessary unless institutions can increase throughput.

Existing update and control cycles may become insufficient

Most financial institutions already operate structured remediation cycles supported by approvals, testing windows, documentation requirements, and governance checkpoints. Those controls exist for good reason. The challenge is that controls designed for slower operating environments may become difficult to sustain if threat discovery accelerates.

This does not mean banks need entirely new frameworks. It means existing Financial Crimes Risk Management processes may need to operate with shorter preparation cycles, faster evidence collection, and more efficient case execution while preserving monitoring.

Risk prioritization becomes more difficult

Faster threat identification creates a less visible challenge. Not every alert deserves immediate escalation. As investigation queues grow, institutions must decide which vulnerabilities, customers, transactions, and cases carry the highest operational and regulatory exposure.

Financial Crimes Risk Management increasingly becomes an exercise in intelligent prioritization rather than maximum investigation coverage. The institutions most likely to perform well may not be those that generate the most alerts. They may be the institutions that can prepare investigations faster, concentrate resources where exposure is highest, and maintain clear decision standards under pressure.

Higher documentation and audit requirements

Greater investigative speed does not reduce accountability because every investigation still requires evidence, rationale, approvals, and traceable decisions. Regulators do not lower expectations because operating environments become more multiplex.

If investigation cycles compress, documentation requirements become even more important because institutions must prove what decisions were made and how those decisions were reached.

That increases pressure on FinCrime compliance teams to maintain explainability, preserve audit trails, and produce consistent investigative outputs even as response expectations accelerate.

What Should European Banks Evaluate and Update in Their Financial Crimes Risk Management Model?

The Mythos instance does not suggest that European banks need to replace their Financial Crimes Risk Management frameworks. Instead, it highlights that existing operating models may need to respond to risks much faster than they were originally designed for.

If AI continues to accelerate threat discovery and analysis, institutions will have less time to investigate exposures. In that environment, adding more technology alone is unlikely to solve the problem. Banks should first assess whether their current Financial Crimes Risk Management operating model can support faster execution without weakening governance.

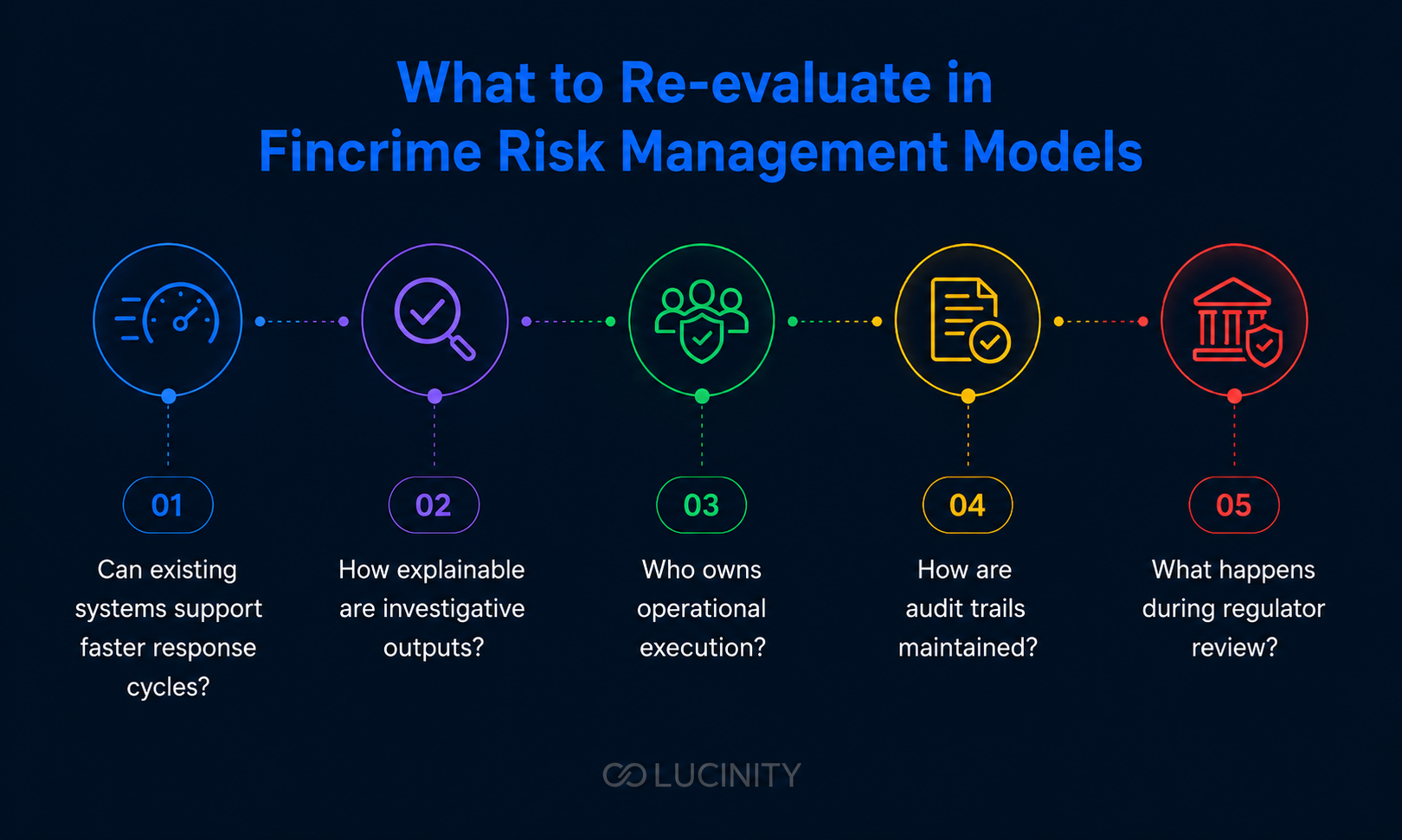

Rather than evaluating solutions based on feature lists, institutions should evaluate whether they improve operational readiness, investigation throughput, and auditability. The following questions provide a practical framework for that assessment:

1. Can existing systems support faster response cycles?

The Mythos case suggests that Financial Crimes Risk Management may soon operate under much shorter response windows. If AI can identify vulnerabilities and analyse potential threats in hours instead of weeks, investigation workflows must be able to keep pace without compromising governance.

Many banks still rely on multiple disconnected systems to gather evidence, review customer information, validate alerts, and document investigative findings. While these processes have supported compliance for years, they can introduce delays when every investigation requires repeated manual effort and coordination across teams.

Instead of replacing existing infrastructure, institutions should evaluate whether their current operating environment can support faster execution. Questions such as how many systems investigators use, how much time is spent preparing cases, and whether throughput can increase without adding headcount become increasingly important as Financial Crimes Risk Management adapts to shorter operating cycles.

2. How explainable are investigative outputs?

As AI becomes more involved in identifying risks and supporting investigations, explainability becomes a core requirement rather than a desirable feature. Faster analysis only creates value if investigators, auditors, and regulators can understand how conclusions were reached.

Banks should evaluate whether investigative outputs include clear reasoning, traceable evidence, visible assumptions, consistent documentation, and meaningful human review. These elements help ensure that accelerated workflows do not reduce transparency or weaken governance.

The relevance of Mythos extends beyond speed. It reinforces the need for Financial Crimes Risk Management models that increase investigation efficiency while producing outputs that remain understandable, reviewable, and defensible throughout the investigation lifecycle.

3. Who owns operational execution?

The Mythos discussion also highlights the importance of distinguishing operational execution from regulatory accountability. Faster investigation cycles do not change who remains responsible for decisions, reporting obligations, or supervisory engagement.

Banks should clearly define who prepares investigations, who validates findings, who manages remediation activities, and who approves escalations. Clear ownership prevents operational improvements from creating uncertainty around governance responsibilities or decision-making authority.

As Financial Crimes Risk Management evolves, institutions should ensure that increased execution capacity strengthens existing governance rather than replacing it. Higher throughput delivers value only when accountability remains clearly assigned and consistently applied.

4. How are audit trails maintained?

Compressed investigation timelines increase the importance of maintaining complete and reliable audit trails. Every investigative action should remain traceable regardless of how quickly cases move from detection to remediation.

Banks should be able to reconstruct the evidence reviewed, the reasoning behind each decision, approval history, and the actions taken throughout an investigation. Standardised documentation also helps maintain consistency across teams during periods of increased operational pressure.

Mythos illustrates how AI may accelerate the pace of investigations. Financial Crimes Risk Management therefore requires documentation practices that scale alongside operational speed while continuing to meet supervisory expectations.

5. What happens during regulator review?

Regulators assess more than the outcome of an investigation. They evaluate whether institutions followed appropriate processes, maintained governance standards, and can demonstrate why specific decisions were made.

Banks should therefore consider whether investigation timelines can be reconstructed months later, whether documentation remains consistent across teams, and whether evidence sufficiently supports every remediation decision. These capabilities become increasingly valuable when investigations are completed under strict operational deadlines.

The broader lesson from Mythos is that Financial Crimes Risk Management should be measured not only by how quickly risks are identified but also by how confidently institutions can explain and defend every action taken in response.

Read more on Financial Crimes Risk Management Overhaul

The Importance of Increasing Investigation Capacity Without Compromising Governance

The debates and conversation happening around Mythos highlight a growing challenge for Financial Crimes Risk Management. As threat identification accelerates, banks need to investigate, document, and respond more quickly without compromising governance or regulatory monitoring.

A Human AI operating model helps address this challenge by accelerating investigation preparation while keeping decision-making with the institution. Lucinity delivers this through Agentic FinCrime Services, operating AML and KYC workflows under SLA within a bank's existing systems.

Luci gathers evidence, structures findings, and drafts investigation narratives, enabling analysts to focus on reviewing cases and making informed decisions.This ensures faster investigations without sacrificing explainability or accountability.

Using this approach, institutions have reduced investigation time from 2.5 hours to 30 minutes, achieved up to 90% productivity gains, and lowered operating costs by 60-80% without requiring workflow disruption or system migration.

As Financial Crimes Risk Management continues to evolve, operating models that improve investigation throughput while preserving governance will become increasingly valuable.

Final Thoughts

The discussion around Mythos should not be viewed as a prediction about a single model or a temporary cybersecurity event. It highlights a broader shift that European banks are already starting to experience.

Financial Crimes Risk Management has traditionally focused on improving detection and strengthening controls. Banks that can prepare investigations faster, maintain explainability, and shorten response cycles inside existing environments may be better positioned than institutions relying on detection improvements alone.

- Financial Crimes Risk Management is becoming more dependent on execution speed alongside detection quality.

- Faster threat discovery may expose bottlenecks in investigation and remediation workflows.

- Explainability, audit readiness, and governance remain essential even as response timelines shorten.

- Operating models that increase throughput without disrupting existing systems may become a long-term advantage.

To explore how your organization can align the AML compliance model for the growing AI threats in money laundering, visit Lucinity today!

FAQs

1. How could Mythos influence Financial Crimes Risk Management in European banking?

Mythos highlights how faster risk discovery can pressure existing investigation and remediation cycles, increasing the importance of operational readiness and response capacity.

2. Why is Financial Crimes Risk Management becoming more operational?

Institutions increasingly generate more risk signals than they can process efficiently. Investigation throughput and documented execution are becoming as important as detection.

3. Does faster investigation mean reducing governance controls?

No. Faster operating cycles should improve preparation and execution while keeping approvals, oversight, and regulatory accountability unchanged.

4. How can banks improve Financial Crimes Risk Management without replacing systems?

Banks can improve capacity by reducing preparation bottlenecks, increasing investigation throughput, and operating inside existing environments where possible.

5. What role does explainability play in Financial Crimes Risk Management?

Explainability supports audit readiness and regulatory confidence by making evidence, reasoning, and decisions visible and reviewable.