What Cross-Border Payment Risks Reveal About the Future of AML Compliance Services in Europe

Learn what cross-border payment risks reveal about the future of AML Compliance Services and AML operations in Europe.

Cross-border payments are becoming faster, more accessible, and increasingly embedded into everyday financial activity across Europe. Yet recent enforcement actions across the payment sector suggest that transaction growth alone is not creating the pressure.

One recent European enforcement case showed the institution processed more than €100 billion in annual payment volume but had failures tied to customer due diligence, transaction monitoring, and operational execution

For AML leaders, the question is becoming less about identifying suspicious activity and more about whether investigations, documentation, escalation, and reporting can keep up without increasing cost, difficulty, or governance risk.

This article explores what cross-border payment risks reveal about the future of AML operations in Europe, what institutions should learn from recent market signals, and what modern AML Compliance Services increasingly need to deliver.

Why Have Cross-Border Payments Become an Important AML Challenge in Europe?

Cross-border payments are becoming one of the clearest indicators of how AML operations are changing across Europe because institutions are processing larger transaction volumes across more jurisdictions while customers expect faster experiences. Simultaneously, regulators expect stronger evidence, clearer documentation, and more consistent monitoring.

Recent regulatory action involving a major European cross-border payment institution brought this pressure into focus. Public findings pointed to weaknesses across customer due diligence, transaction monitoring, and AML execution despite substantial operational scale and international growth.

The lesson is that cross-border payment growth exposes how difficult it becomes to maintain investigation quality and operational consistency as difficulty increases.

Cross-Border Transactions Outpaced Transaction Growth

For years, AML capacity planning was largely volume-based. More customers and more transactions generally meant hiring more investigators and expanding monitoring coverage.

Cross-border activity changes that model. Transaction growth now arrives together with greater jurisdictional exposure, more customer variation, and increased documentation requirements. The effort required to understand activity often grows faster than the transaction count itself.

A single payment can involve multiple countries, currencies, counterparties, payment rails, ownership structures, and regulatory obligations. That means investigation efforts have become increasingly concentrated around context gathering rather than decision-making. Teams spend more time preparing cases before meaningful review can even begin.

Fragmented Data Creates Investigation Friction

Cross-border payments rarely arrive with complete context in one environment. Investigators often need to combine:

- Transaction history

- Customer due diligence records

- Ownership structures

- Sanctions and screening outputs

- Historical behavior

- External supporting information

When these inputs remain distributed across systems, preparation becomes slow and inconsistent. This challenge compounds over time.

Every additional manual step increases review time, creates documentation variation, and reduces the number of investigations teams can complete with the same resources. As payment activity accelerates, fragmented workflows become increasingly difficult to sustain.

Regulatory Expectations Are Expanding Beyond Detection

European AML expectations increasingly evaluate whether suspicious activity was identified and whether institutions can explain how conclusions were reached. Regulators increasingly expect institutions to demonstrate:

- What Information Informed Decisions,

- Whether Investigative Reasoning Was Documented,

- Whether Reviews Followed Established Governance,

- Whether Decisions Remain Traceable Through Audit.

This raises the operational standard. An institution may detect suspicious activity correctly and still face scrutiny if investigative processes appear inconsistent or insufficiently documented. The quality of execution becomes part of the compliance outcome.

Operational Capacity Is Emerging as the Real Constraint

The result of these combined pressures is that AML teams are increasingly constrained by execution capacity rather than monitoring capability. More alerts created:

- More preparation work.

- More investigation time.

- More documentation requirements.

- More quality assurance.

- More escalation management.

This explains why institutions across Europe are reassessing AML Compliance Services. The discussion is gradually shifting away from who generates alerts most effectively and toward who can prepare, investigate, document, and complete cases with consistency at scale.

Cross-border payment risk is revealing a broader operational reality. The future of AML operations in Europe will likely depend less on detecting more activity and more on sustaining investigation throughput, regulatory confidence, and operational resilience as financial activity becomes increasingly connected.

How Cross-Border Payment Risks Are Changing AML Approaches

Cross-border payment growth is forcing institutions to rethink several assumptions that shaped AML operations over the last decade.

For many years, compliance programs were designed around relatively stable transaction environments. Growth was expected to follow a familiar pattern. Transaction volumes increased, teams expanded, controls matured, and operating capacity gradually followed.

Cross-border payment environments challenge those assumptions. What recent market signals increasingly show is that scale alone does not guarantee stronger compliance outcomes. Instead, institutions are reassessing how AML work should be organized, executed, and governed.

From Monitoring Coverage to Operational Outcomes

Historically, many AML programs measured maturity through coverage. Questions often focused on:

- How many scenarios exist?

- How many alerts are generated?

- How many controls are active?

- How broad is screening coverage?

Those measures still matter. However, cross-border environments introduce a second question. Can institutions consistently convert alerts into documented, explainable decisions?

As transaction movement becomes faster and customer activity becomes more international, operational outcomes become increasingly visible. The ability to complete investigations consistently starts carrying equal weight to the ability to identify potential risk.

From Staffing Models to Capacity Models

Cross-border activity is changing how institutions think about scale. Traditional growth often meant:

- Larger analyst teams

- Expanded review functions

- Additional quality controls

That model becomes harder to sustain when payment growth outpaces hiring capacity and regulatory expectations continue expanding. As a result, institutions are increasingly shifting from workforce expansion to capacity planning.

The discussion becomes less about adding reviewers and more about questions such as:

- How much work can operations complete?

- How quickly can investigations move?

- How consistent are outcomes?

- How resilient is execution during volume spikes?

This changes attention toward operating design rather than organization size.

From Internal Ownership to Shared Operational Execution

Another shift emerging across Europe is the distinction between governance and execution. Historically, institutions often assumed retaining regulatory ownership required retaining every operational task internally.

Cross-border payment environments are challenging that assumption.

Institutions increasingly separate:

- Regulatory accountability

- Governance decisions

- Operational execution

- Investigation preparation.

This allows institutions to strengthen throughput and consistency while maintaining oversight and approval authority. The objective is not reducing control. It is preserving control while improving execution.

From Compliance Infrastructure to Compliance Performance

Cross-border risk is also changing how success is evaluated. Institutions increasingly want evidence that AML operations can:

- Remain stable under growth.

- Maintain documentation quality.

- Support audits.

- Adapt without disruption.

- Sustain performance over time.

This changes the role of AML Compliance Services. The conversation increasingly moves beyond technology procurement and toward operational performance.

Cross-border payment risk is revealing that future AML advantage may come less from building more infrastructure and more from building operating models capable of sustaining trust, oversight, and execution as financial activity continues to expand.

How Are European Institutions Adapting AML Operations to Support Cross-Border Growth?

As cross-border payment activity expands, institutions across Europe are making a broader adjustment than introducing additional controls or expanding investigation teams.

Payment growth, faster transaction movement, and more fragmented customer activity are creating pressure that cannot always be absorbed through hiring or incremental process changes. Institutions are increasingly reassessing how investigations are prepared, executed, and governed.

The objective is becoming more consistent execution under growing transaction volumes and regulatory expectations. These changes are taking shape across several key areas of AML operations, particularly in how institutions manage capacity and structure investigations.

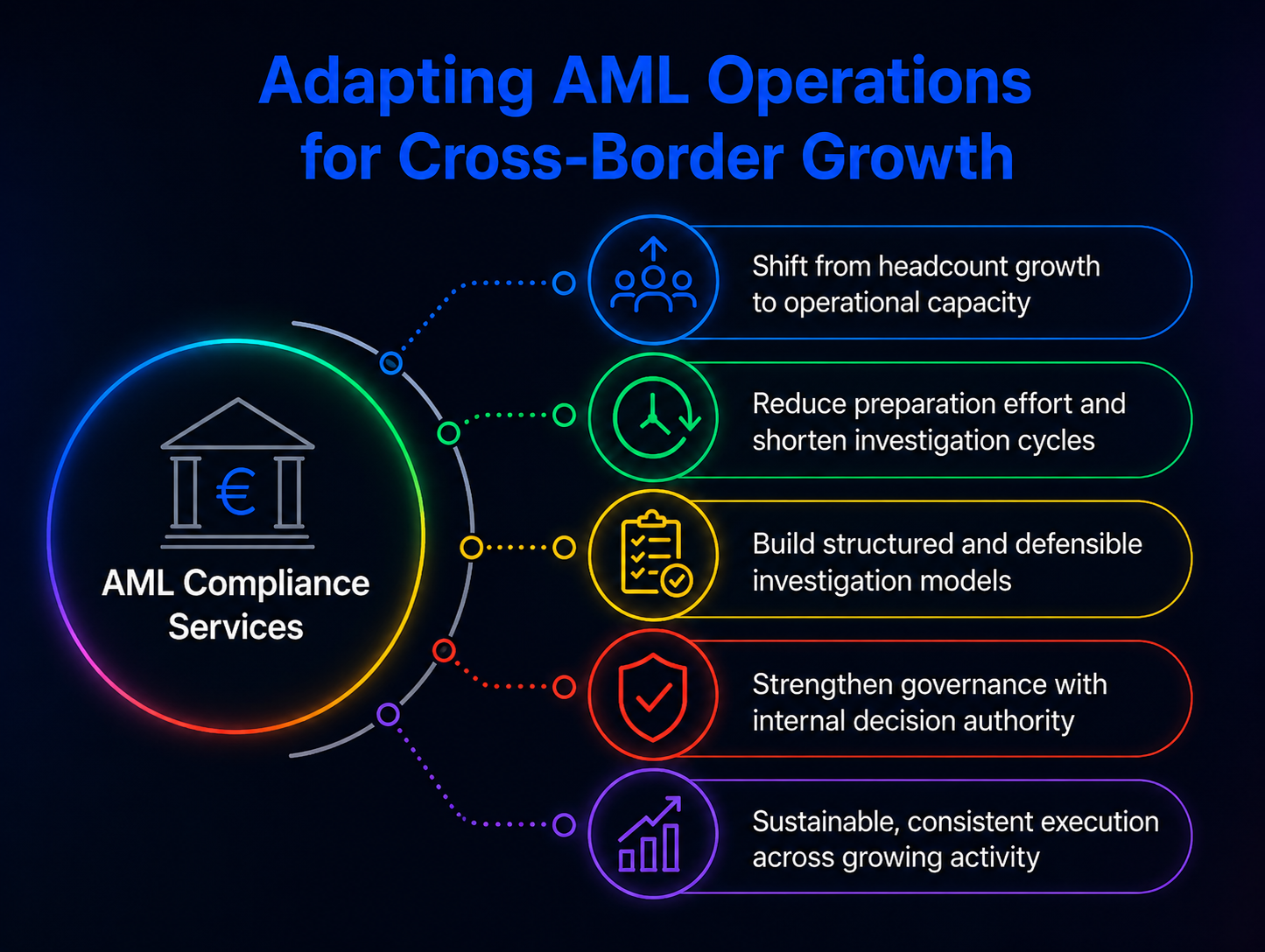

Moving From Workforce Expansion to Operational Capacity

For many institutions, AML growth historically followed a familiar pattern. More transactions generated more alerts, and more alerts required more analysts. Cross-border environments are making that model harder to sustain.

Transaction difficulty does not increase in a straight line. Additional markets, payment corridors, customer types, and documentation expectations often create disproportionately larger investigation workloads.

As a result, institutions are placing greater emphasis on operational capacity. This means improving how work gets completed rather than simply increasing the number of people performing it.

Current priorities increasingly include:

- Reducing case preparation effort.

- Shortening investigation cycles.

- Improving consistency.

- Increasing completed investigations without proportional headcount growth.

The goal is enabling investigators to spend more time reviewing and less time assembling information.

Building More Structured and Defensible Investigation Models

Cross-border growth is also changing how institutions think about investigation quality. As reviews become more difficult, institutions are placing greater emphasis on structure and consistency across operations.

This includes:

- Clearer evidence collection standards.

- More repeatable investigation workflows.

- Stronger documentation practices.

- Easier supervisory review.

The aim is to make investigations easier to understand, validate, and defend. Simultaneously, institutions continue drawing a clear line around governance. Operational execution may evolve, but decision authority remains internal.

Approval thresholds, escalation rules, reporting obligations, and regulatory accountability continue to stay with the institution. This distinction is increasingly shaping expectations around AML Compliance Services.

The institutions adapting most effectively are not reducing oversight or lowering standards. They are redesigning execution so investigations remain sustainable as cross-border activity becomes larger, faster, and more interconnected.

How Lucinity Supports Cross-Border AML Operations Without Disrupting Governance

As cross-border payment volumes grow, institutions are under pressure to increase investigation capacity without changing governance structures or creating operational disruption.

Lucinity addresses this as a Human AI operator rather than a software vendor or traditional outsourcing provider. AML and KYC operations are executed under SLA inside the client’s existing systems while institutions retain full ownership of decisions, approvals, thresholds, and regulatory accountability.

The model focuses on separating workload from governance. Luci supports investigation preparation by gathering evidence, organizing information, analyzing customer behavior, and drafting structured case narratives before human review takes place.

Human investigators then complete cases according to institutional standards and return outcomes inside the existing environment. This approach allows institutions to increase throughput and consistency without changing how decisions are made.

Across operations, Lucinity has helped reduce average investigation time from 2.5 hours to 30 minutes, with productivity improvements of up to 90% and operating cost reductions of 60 to 80% depending on the engagement model. Every action remains explainable, reviewable, and auditable.

As AML Compliance services continue evolving across Europe, institutions are increasingly looking for operating models that improve execution capacity while keeping governance exactly where it belongs.

Final Thoughts

Cross-border payment risk is becoming one of the clearest signals that AML operations in Europe are entering a different phase. The challenge is no longer limited to identifying suspicious activity. Institutions are increasingly expected to investigate faster, document more consistently, and maintain stronger oversight across larger and more interconnected payment environments.

As cross-border activity continues to expand, the ability to sustain investigation quality, audit confidence, and operational resilience may become a stronger differentiator than monitoring breadth alone.

- Cross-border payment growth is increasing investigation difficulty faster than transaction volume alone suggests.

- Institutions are shifting attention from monitoring coverage toward execution quality and operational capacity.

- Modern AML Compliance Services increasingly depend on explainability, throughput, and governance retention.

- Future AML operating models will likely focus on scaling execution while keeping decisions and regulatory accountability inside the institution.

FAQs

1. What are AML Compliance Services?

AML Compliance Services support financial institutions in investigating suspicious activity, maintaining documentation standards, and meeting regulatory obligations through structured operational execution.

2. Why are cross-border payments increasing pressure on AML Compliance Services?

Cross-border payments introduce more jurisdictions, customer difficulty, and documentation requirements, increasing investigation effort and operational workload.

3. How are AML Compliance Services changing in Europe?

AML Compliance Services are increasingly focusing on execution quality, investigation throughput, explainability, and maintaining governance while improving operational capacity.

4. Does improving AML operations require changing governance structures?

Not necessarily. Many institutions are separating operational execution from governance, so oversight and regulatory accountability remain unchanged.

5. What capabilities should institutions prioritize in future AML operating models?

Institutions increasingly prioritize investigation capacity, structured documentation, audit readiness, explainability, and the ability to operate within existing environments.